Low-emission hydrogen, especially green hydrogen produced from renewable sources, is becoming one of the main global bets for decarbonizing hard-to-electrify sectors such as heavy industry, freight transport, and aviation. Driven by the pursuit of climate neutrality, governments and companies have increased investments and pilot projects in this sector. However, despite the enthusiasm surrounding the “hydrogen economy,” substantial challenges remain to be overcome, particularly related to production costs, regulation, and infrastructure.

Today, Europe, the United States, and China stand out as epicenters of the new hydrogen economy. Europe leads in terms of announced projects, accounting for around 35% of global investments projected through 2030, driven by national strategies, foundational investments in the North Sea, and partnerships with exporting regions such as North Africa (HYDROGEN COUNCIL, 2023). In the United States, the Inflation Reduction Act (IRA) has stimulated strong growth in projects with committed investments, positioning the country as a leader in final investment decisions. China, in turn, has the largest installed electrolysis capacity, with over 780 MW, and is rapidly deploying large-scale projects, benefiting from lower capital costs and strong state support (IEA, 2022). Other regions with abundant natural resources, such as Chile, Saudi Arabia, Australia, and the United Arab Emirates, are also strategically positioned to produce low-cost hydrogen for export.

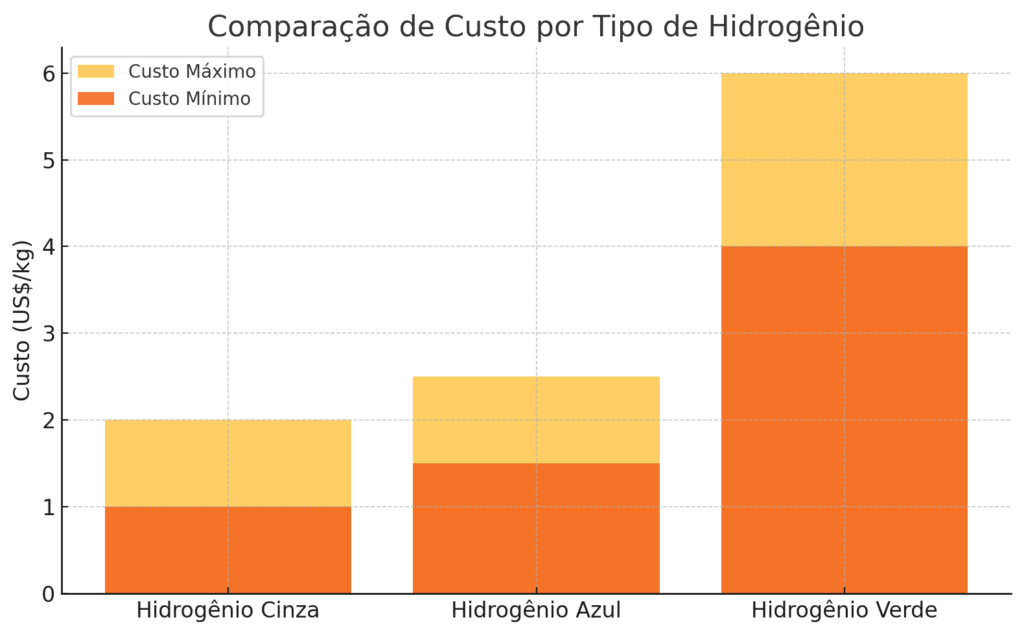

Green hydrogen production is based on water electrolysis powered by renewable energy. Projects may be grid-connected or rely on dedicated solar and wind power plants, often with batteries to manage intermittency. Electrolysis technologies vary between alkaline, PEM, and solid oxide, each at different maturity levels and costs. Currently, the cost of green hydrogen ranges from US$ 4 to 6 per kg, which is higher than gray hydrogen (derived from fossil fuels), whose production accounts for 98% of the global market (IEA, 2022). The challenges include the cost of renewable electricity, the need for scalability, water availability, and high initial investment. A significant cost reduction is expected by 2030 due to cheaper electrolyzers, greater efficiency, and more affordable electricity (BLOOMBERGNEF, 2023).

Below is a visual comparison of the estimated costs by type of hydrogen, highlighting the significant difference between gray, blue, and green hydrogen routes:

On the other hand, blue hydrogen, produced from natural gas with carbon capture and storage (CCS), may be more competitive in the short term, especially in regions with cheap gas and available CCS infrastructure. However, its acceptance depends on increasingly stringent environmental regulations and involves fugitive methane emissions. The competition between green and blue hydrogen is shaped by a constantly evolving political and regulatory landscape, in which the definition of “clean” hydrogen varies between jurisdictions (IRENA, 2022).

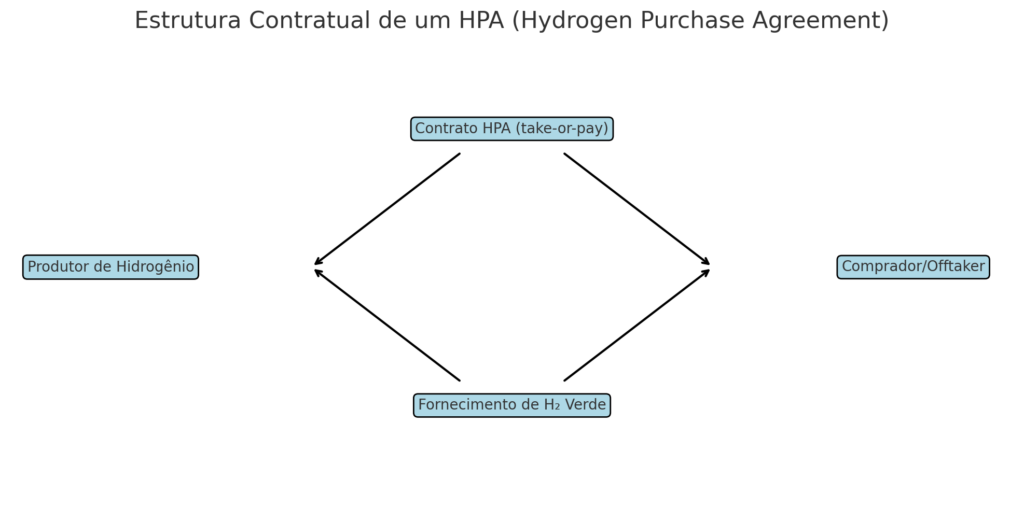

In this context, emerging business models are key to enabling projects. The use of long-term purchase and sale agreements, such as HPAs (Hydrogen Purchase Agreements), inspired by power purchase agreements (PPAs), is essential to ensure revenue predictability. These contracts are typically structured with take-or-pay clauses, guaranteeing payment even if the hydrogen is not physically withdrawn by the buyer. In many cases, prices are calculated based on production costs plus a margin or indexed to the cost of electricity, given that there is not yet a consolidated spot market for hydrogen (NORTON ROSE FULBRIGHT, 2023). The trend is for HPAs to follow LNG market models, with make-up options, indexation, price review, and logistics inclusions.

Below is a simplified diagram of the contractual structure of an HPA:

Real-world cases already demonstrate how these models are being implemented. In Puertollano, Spain, Iberdrola and Fertiberia partnered to produce green hydrogen from solar energy and use it in fertilizer production, with a long-term offtake agreement (IBERDROLA, 2023). In Saudi Arabia, the NEOM megaproject, led by Air Products, plans to export green ammonia under a 30-year exclusive contract (AIR PRODUCTS, 2023). In China, Baofeng Energy integrates hydrogen production into its industrial processes for internal use (BAOFENG, 2023). In Chile, the Haru Oni project converts green hydrogen into synthetic fuels with Porsche’s support (SIEMENS ENERGY, 2023). In Denmark, the HySynergy project supplies green hydrogen to a refinery and monetizes the residual oxygen (EVERFUEL, 2023).

These projects share common elements: vertical integration, long-term contracts, state support, and strategic locations. In Brazil, the potential for green hydrogen is significant, given the predominantly renewable electricity matrix and the abundance of natural resources. States like Ceará, Rio de Janeiro, and Rio Grande do Sul already host pilot projects and memoranda of understanding with foreign companies interested in producing and exporting green hydrogen via strategic ports like Pecém and Açu. The country is positioning itself as a future exporter to Europe and Asia, although it still lacks specific regulatory frameworks and structured public policies for international competitiveness. The inclusion of hydrogen in the National Energy Transition Policy and Petrobras’ plans to invest in green hydrogen (H2V) projects are positive signs. Still, the challenge lies in converting technical potential into financially viable projects integrated into global value chains. These projects also face operational challenges such as energy intermittency, partner synergies, hydrogen origin certification, and transport logistics. Strategically, investors must manage uncertainties related to future demand, regulation, political risks, and technological developments. Choosing modular projects, using derivatives like ammonia or methanol, and geographic diversification are ways to mitigate risks and seize opportunities.

The success of this new hydrogen economy will depend on the ability to build robust business models capable of enduring the high-cost, low-liquidity phase of the market. The key lies in negotiating smart contracts, forming strategic alliances, and aligning investors’ economic goals with global sustainability targets. Pioneering projects already show promising pathways and demonstrate that with appropriate legal structures, efficient management, and long-term vision, hydrogen can move from promise to concrete solution in the energy transition.

References

AIR PRODUCTS. NEOM Green Hydrogen Project. Available at: https://www.airproducts.com/energy-transition/neom-green-hydrogen-complex. Accessed: Mar. 27, 2025.

BAOFENG ENERGY. Hydrogen Project Documentation. Available at: https://www.baofengenergy.com. Accessed: Mar. 27, 2025.

BLOOMBERGNEF. Clean Hydrogen Market Outlook. 2023. Available at: https://about.bnef.com/blog/clean-hydrogen-market-outlook. Accessed: Mar. 27, 2025.

EVERFUEL. HySynergy Project Overview. 2023. Available at: https://www.everfuel.com/hysynergy. Accessed: Mar. 27, 2025.

HYDROGEN COUNCIL. Hydrogen Insights 2023. Available at: https://hydrogencouncil.com/en/hydrogen-insights-2023. Accessed: Mar. 27, 2025.

IBERDROLA. Puertollano Green Hydrogen Plant. 2023. Available at: https://www.iberdrola.com/innovation/green-hydrogen-plant-puertollano. Accessed: Mar. 27, 2025.

IEA. Global Hydrogen Review 2022. International Energy Agency. Available at: https://www.iea.org/reports/global-hydrogen-review-2022. Accessed: Mar. 27, 2025.

IRENA. Geopolitics of the Energy Transformation: The Hydrogen Factor. International Renewable Energy Agency, 2022. Available at: https://www.irena.org/publications/2022/Jan/Geopolitics-of-the-Energy-Transformation-Hydrogen. Accessed: Mar. 27, 2025.

NORTON ROSE FULBRIGHT. Hydrogen Offtake Agreements: Legal Considerations. 2023. Available at: https://www.nortonrosefulbright.com/en/knowledge/publications/83d40c3d/hydrogen-offtake-agreements. Accessed: Mar. 27, 2025.

SIEMENS ENERGY. Haru Oni Pilot Project. 2023. Available at: https://www.siemens-energy.com/global/en/news/magazine/2022/pilot-project-haru-oni.html. Accessed: Mar. 27, 2025.